Are you constantly inclined towards parking your surplus funds in safe instruments like fixed deposits? What if a better option exists that gives you best of both worlds i.e. safety like FDs and better returns too.

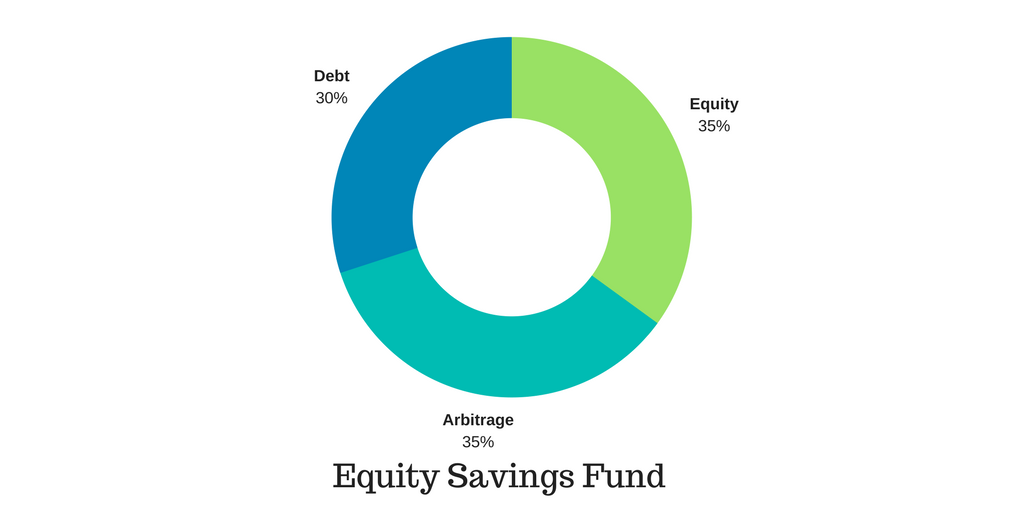

Mutual funds have introduced ‘Equity Savings Fund’ that distribute its investment between debt, arbitrage, and equity asset classes. Usually, 30%-40% of the total corpus is allocated towards equity, consisting mainly of large cap stocks that helps keep the portfolio stable. Another 30%-40% is invested in arbitrage and remaining goes into debt.

Alternatively, you can opt for ‘Equity income fund’ to further reduce your equity exposure to 20%, focussed on large-cap stocks. The fund allocates 45% into arbitrage and the balance in debt.

Equity savings fund vs fixed deposits

Apart from better returns, equity savings fund scores over fixed deposits on other fronts as well.

Taxation - It is common knowledge that the interest earned on fixed deposits is taxable, hence, post-tax returns can drop substantially if an individual falls into a higher tax bracket. On the flip side, equity savings fund enjoy tax-status of equity funds. This implies that investment in these funds for over a year will be accounted as long-term capital gains that are not taxable. Investments for less than a year are taxed as short-term capital gain at 15%.

Inflation - An investment makes sense only if it is successful in fetching returns over and above inflation. The real gain occurs when the returns beat inflation. Currently, the inflation rate is hovering around 6% p.a. that makes returns from fixed deposits in the range of 7%-8% unattractive. Moreover, the tax impact further ruins the return potential of deposits. Conversely, equity savings fund has been able to deliver double-digit returns over one year period that smartly beats inflation.

Equity savings fund vs other asset classes

It is important to understand how equity savings fund fare against not just fixed deposits but also other asset classes. The same is put together in a table below for a better understanding.

Asset Class

|

Pros

|

Cons

|

Debt Funds

|

A higher debt portion makes it relatively safe. |

|

Hybrid Funds (Debt Oriented)

|

Safer option alongside some exposure to equity. | Tax applicable as per slab rate for holding period of less than 3 Years |

Equity Funds

|

Promising returns in long-term. | High risk involved for short-term investments |

Equity Savings Fund

|

|

Diminishing returns from arbitrage portfolio during market down phase. |

Ideal investment period

Investment in certain funds works best if they are made for the right investment horizon. From this perspective, equity savings fund qualify to be a part of a portfolio if the investment tenure is more than one year. Anything below the said time horizon will attract tax and will be counterproductive.

About The Author: Reenika Avasthi is associated with Inverika Investment Solutions LLP as a Content Writer and Financial Planner. She is a Certified Financial Planner and a freelance content writer in the field of personal finance. Her interest in writing and spreading investor awareness motivated her to start blogging.

No comments:

Post a Comment